Banks not lending like they used to has become one of the biggest quiet shifts in the mortgage market in the last twenty years. A recent Yahoo Finance article reported that the Fed is considering changes to mortgage lending rules to encourage banks back into the business. It is a sign that the structure of the mortgage market changed enough that regulators are now openly talking about how to bring banks back into the game.

For the last few years, too much of the industry has been sitting around waiting for rates alone to fix affordability. While many have been holding their breath, credit unions have been doing what the market actually needs: building solutions, serving niche borrowers, and growing in a market that still feels locked-in.

Why Are Banks Not Lending Like Before?

When most people talk about affordability, they talk about rates first. Rates matter, but they are not the whole story.

The larger issue is that banks not lending as aggressively as they once did has changed who fills the gap for borrowers. Traditional banks used to dominate mortgage origination and servicing. After the financial crisis, the Dodd-Frank Wall Street reform act, that shifted. According to the same Yahoo Finance report, the Fed is now exploring whether regulatory changes could make mortgage lending more attractive for banks again.

If policymakers are discussing ways to bring banks back, that means the market has already moved.

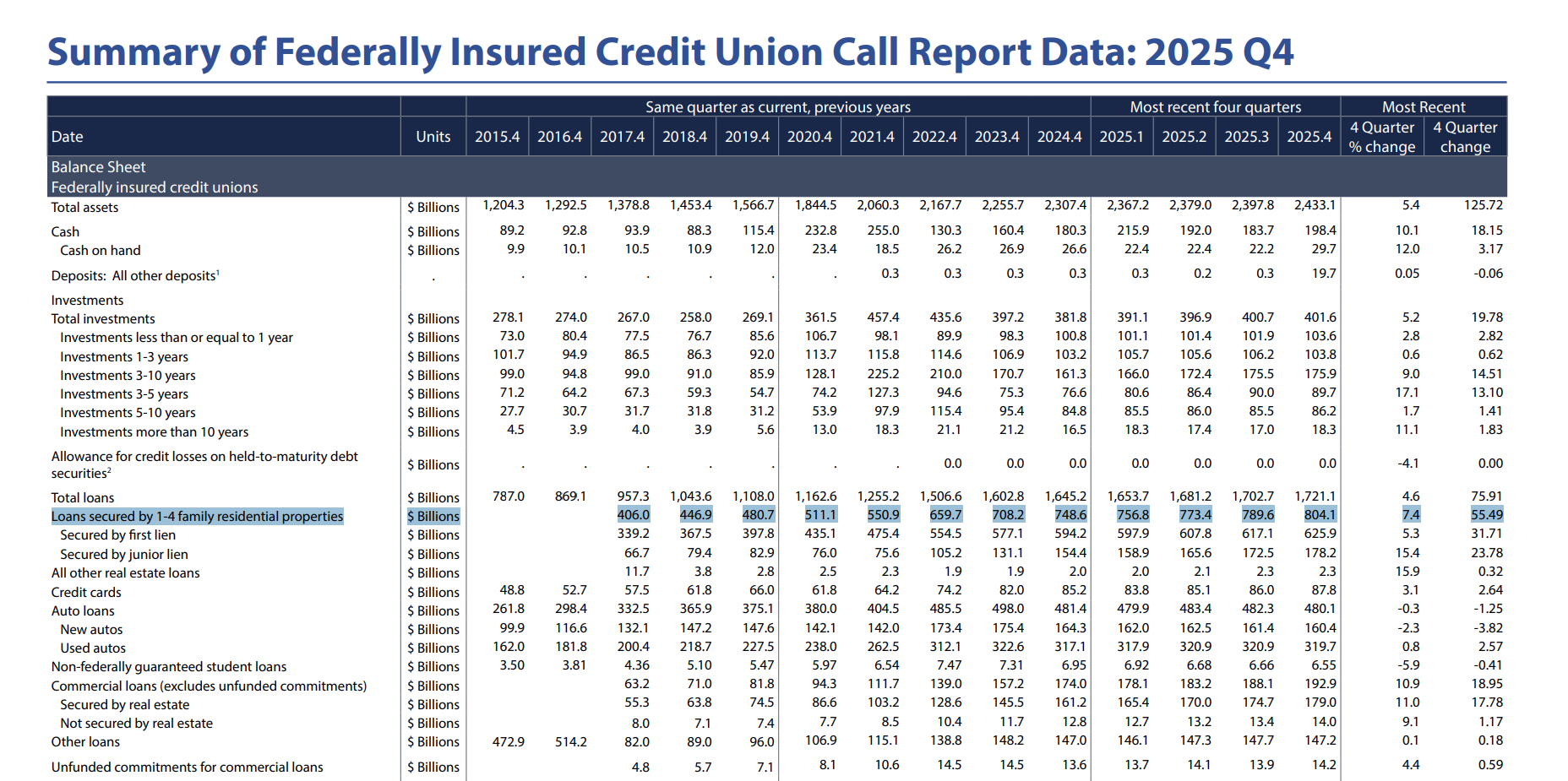

As banks not lending at past levels reshaped the market, NCUA data show credit union 1-4 family mortgage balances grew from $406.0B to $804.1B from 2017 Q4 to 2025 Q4.

Banks Not Lending Created Room for Credit Unions

This is where credit unions come in.

While the broader market waits for a perfect rate environment, credit unions have been quietly increasing their role in mortgage lending. The NCUA Quarterly Data Summary for 2025 Q4 shows that loans secured by 1-4 family residential properties at federally insured credit unions rose from $406.0 billion in 2017 Q4 to $804.1 billion in 2025 Q4.

That is an increase of $398.1 billion, or roughly 98%, in eight years.

So when people ask what happens with banks not lending at prior levels, the answer is simple: someone else steps in. Right now, credit unions are proving they can do that inside a regulated, member-focused model.

Banks Not Lending Is Opening the Door for a Different Kind of Lender

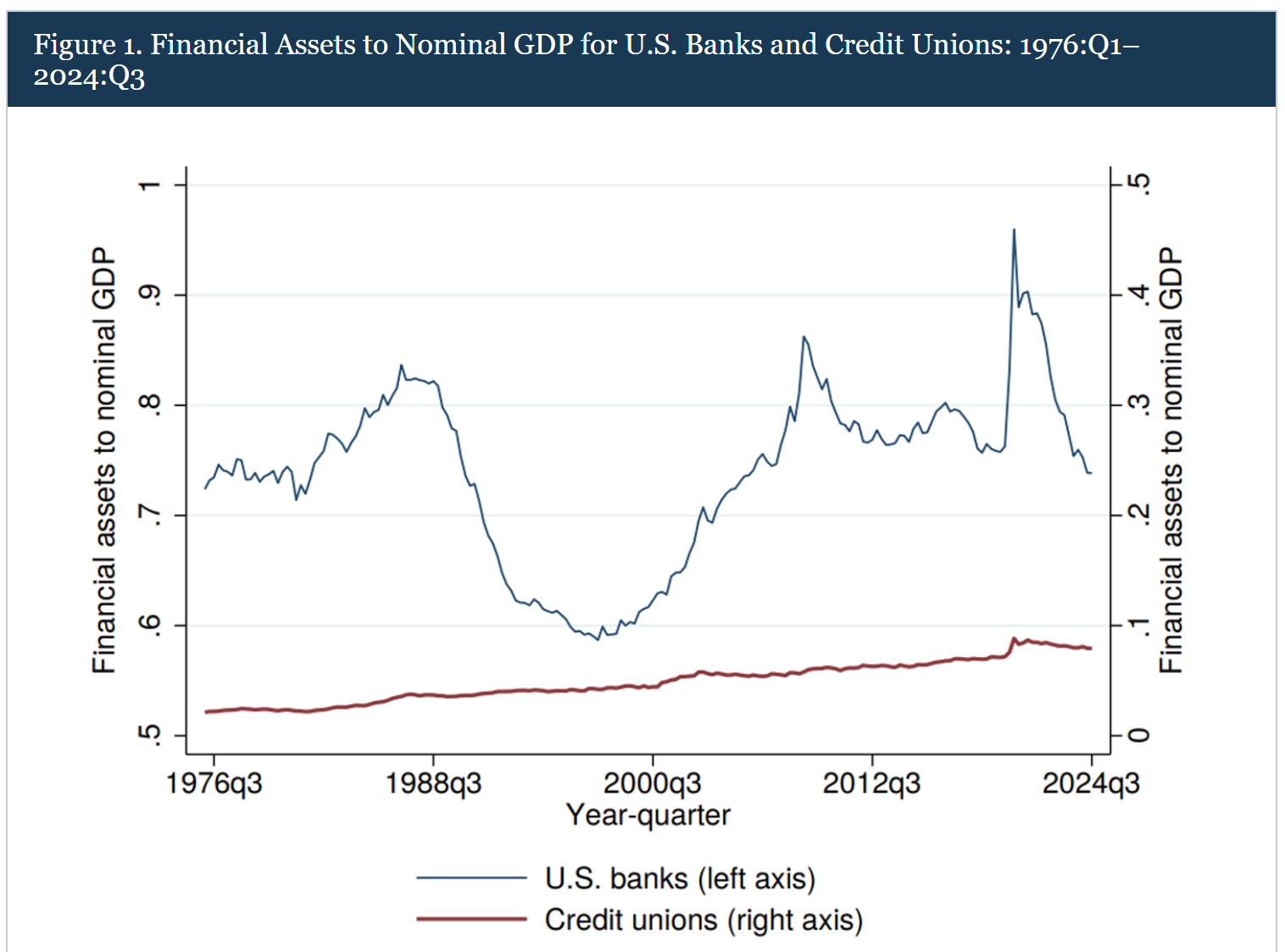

There is a longer trend underneath all of this. The Federal Reserve note on credit unions’ share of household lending shows that credit unions have been playing an increasingly important role in mortgage lending over time. The Fed found that credit union one-to-four-family mortgage holdings rose from less than 1% of GDP in 1990 Q1 to about 2.6% of GDP in 2024 Q3.

That is not a one-year blip. That is a dent in the mortgage universe.

In a market defined by affordability strain, limited inventory, and locked-in sellers, that trend matters. Banks not lending like they used to has created room for other lenders to gain relevance, and credit unions have been taking that opening seriously.

Federal Reserve chart showing financial assets to nominal GDP for U.S. banks and credit unions from 1976 Q1 to 2024 Q3, illustrating the steady long-term rise of credit unions. Source: Federal Reserve, Trends in Credit Unions’ Share of U.S. Private Depository Household Lending.

Banks Not Lending Feels Like the Market Shift Before the Breakout

This is where I cannot help but think of the Southern underground rap scene from the early 2000s.

The major labels were still the majors. They had the infrastructure, the money, and the advances. But the real movement was home grown. It had more grit, a local sound, and more connection to what people actually wanted. Then one day the underground was not underground anymore. I t had become too big and too loud to ignore.

That is what credit unions feel like in mortgage right now.

Not underground in the shady sense. Underground in the sense that they have been underestimated while steadily building traction. Plenty of whoop, and less trick.

What Banks Not Lending Means for Borrowers

If banks not lending sounds like an industry problem, it is really a borrower problem first.

Borrowers still need answers. They need financing structures that reflect real life, not just ideal conditions. They need lenders that can work through construction scenarios, professional-income borrowers, affordability pressure, and situations where the standard box does not fit.

That is where credit unions have room to keep growing. They are not waiting around for a rescue. They are building volume while much of the market is still waiting for the environment to improve.

The NCUA data back that up, and the Federal Reserve’s long-term analysis shows this is not just a temporary reaction. It is part of a larger shift in the lending landscape.

How Borrow Buy Build Fits In

At Borrow Buy Build, this matters because we operate in the part of the market where borrowers need more than generic advice.

You can connect this article to other parts of your site with a few internal references like these:

Read more about our [construction and lot loans] for buyers who need a path beyond the standard resale mortgage.

Explore our [physician mortgage programs] for high-income professionals who need lending built around real-world income timing and career structure.

See our [home affordability article] for strategies that go beyond simply waiting for rates to fall.

Review our [build budget calculator] for borrowers wanting to map out the input costs.

Famous Last Words

The big takeaway is not just that regulators want banks to do more. The bigger takeaway is that while the market debates how to rebuild the past, credit unions are building in the present.

Banks not lending at prior levels has opened the door for a different kind of mortgage player to gain ground. Credit unions are not waiting around for a rescue. They are turned up, in the best way – gaining relevance, and proving that practical lending solutions still matter in a market that feels locked up.

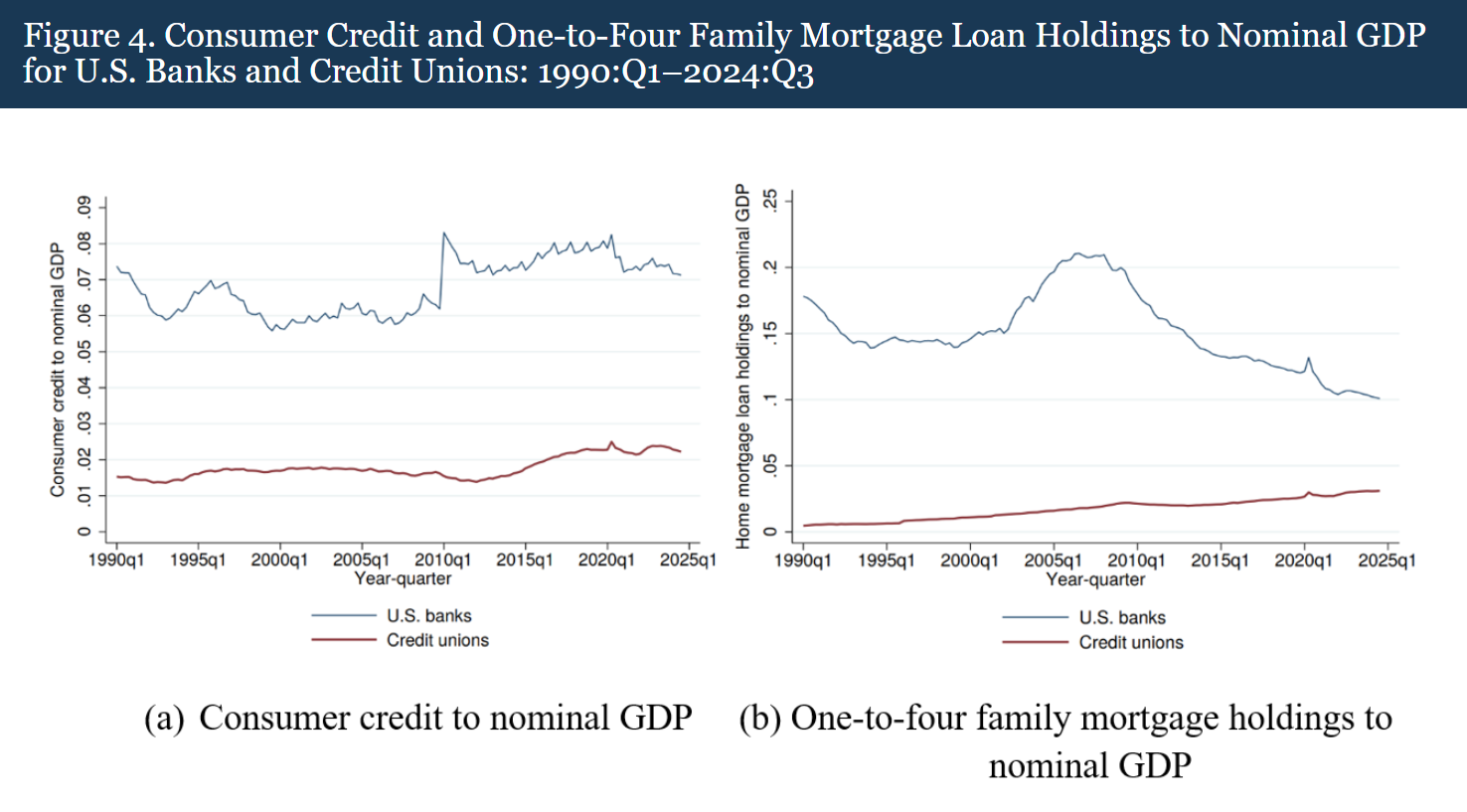

Federal Reserve chart showing consumer credit and one-to-four family mortgage loan holdings to nominal GDP for U.S. banks and credit unions from 1990 Q1 to 2024 Q3. Source: Federal Reserve, Trends in Credit Unions’ Share of U.S. Private Depository Household Lending.