Builder incentives are still one of the biggest conversations in the new home market.

Some buyers are offered closing cost credits, some are offered temporary payment relief, while others are offered a permanent rate buydown. That’s a lot of math to answer for the model home tour.

So what works best for use of the builder incentive, immediate lower payment relief, or a permanent buydown for the long haul? Moreover, do they promise a refinance later?

Great questions in any market, but perfect for 2026.

Mortgage rates surged in 2022. Since the peak of 8% mortgage rates, they have improved, but remain inside a choppy 6% to 7% range. That means a refinance opportunity could exist, but it may not be dramatic enough to automatically beat a permanent buydown. So why not test it, and that is what we did!

First, let’s use a real world figures starting in May 2024, when the 30 year fixed was around 7%. Then we will compare what happened by mid-May 2026, where the market rate hovers around 6.375% for this illustration.

The goal is to review the math and show a contrast between the 2-1 Buydown vs Permanent Buydown. What was your total payout, your equity today, and how to respond to future (lower) interest rates.

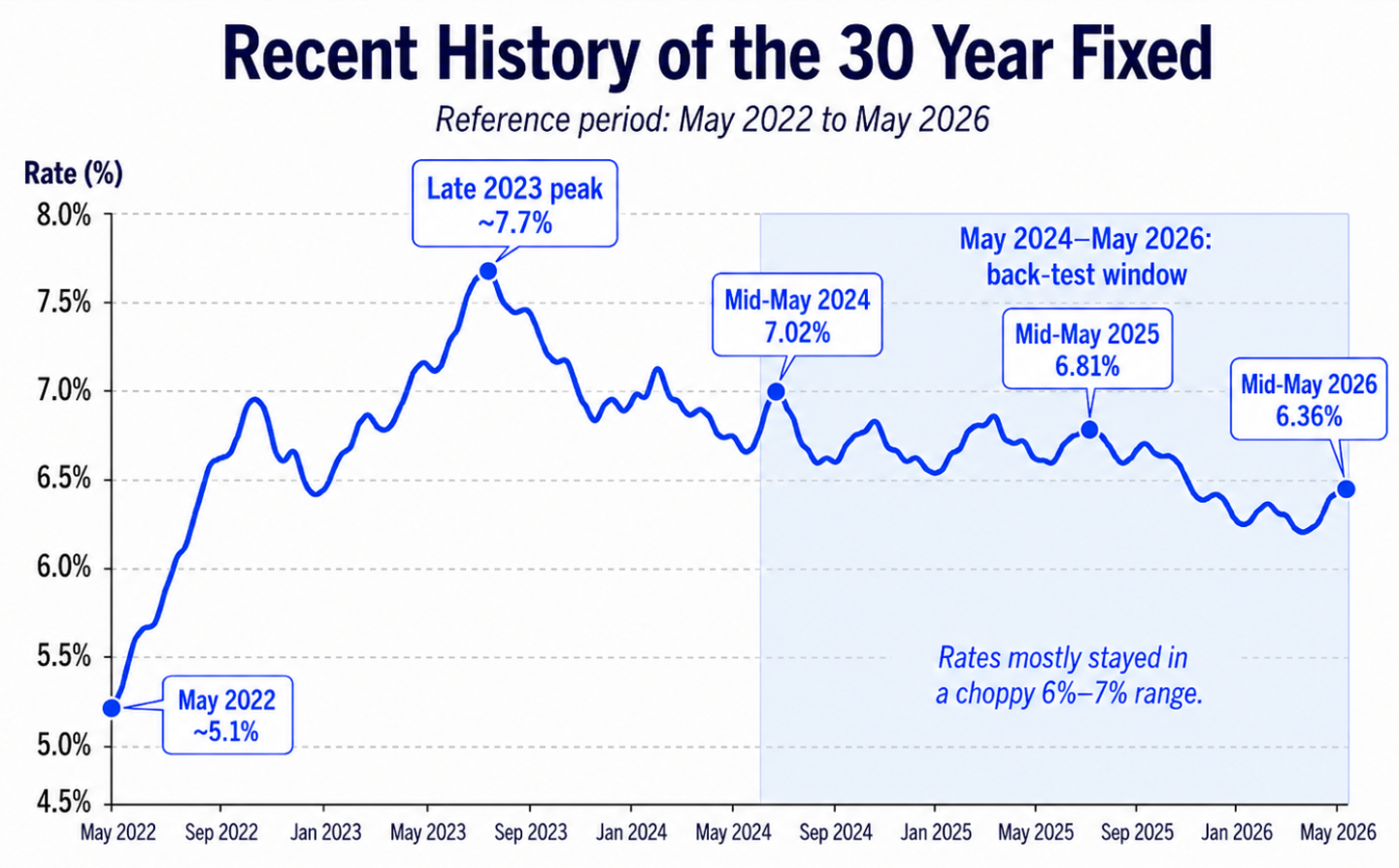

Recent History of the 30-Year Fixed

Freddie Mac’s Primary Mortgage Market Survey reported the 30 year fixed at 7.02% in mid-May 2024 and 6.81% in mid-May 2025. The PMMS archive also showed the 30-year fixed at 6.36% in mid-May 2026. You can also view the longer historical trend through the Federal Reserve Bank of St. Louis on the FRED 30-Year Fixed Rate Mortgage Average.

For this exercise, I am rounding the May 2024 starting point to 7.000% and using 6.375% for the May 2026 refinance rate.

The Question Worth Testing

Say you purchased your new home and closed May 2024. The months leading up to it may have presented a few choices.

You could have taken a “temporary” 2-1 buydown based on a 7% note rate. That would make the first year payment feel like 5%, the second year payment feel like 6%, and then the payment would return to the full 7% note rate in year three.

Second option, use the builder incentive toward a permanent buydown, lowering the actual note rate to 6.625%.

Just to muddy the waters…let’s assume you completed the the 2-1 buydown, enjoyed the lower payment for two years, and then refinanced in May 2026 at 6.375%*. Assume the costs of the refinance was $2,000 and rolled into the loan.

That third option is the one a lot of buyers had in mind in 2024. So let’s go to the video tape!

First, the “Assumptions” for the Example

To keep the math clean, I am using a $100,000 loan amount.

This is not meant to quote today’s exact pricing. It is an illustration to compare strategy.

| Assumption | Amount |

|---|---|

| Loan amount | $100,000 |

| Original term | 30 years |

| Original market note rate | 7.000% |

| 2-1 buydown year-one payment rate | 5.000% |

| 2-1 buydown year-two payment rate | 6.000% |

| Permanent buydown rate | 6.625% |

| May 2026 refinance rate | 6.375% |

| Refinance timing | After 24 months |

| Refinance costs | $2,000 rolled into new loan |

| New refinance term | 28 years remaining |

* One important note on the permanent buydown. In a normal market, one discount point often moves the rate by about 0.25%, but that relationship is not fixed. Pricing changes daily with market conditions. The Consumer Financial Protection Bureau has a helpful explanation of discount points and lender credits if you want the consumer facing version of how points work.

For this example, I am assuming a generous builder or lender incentive that gets the permanent buydown to 6.625%, which is a healthy 0.375% below the original 7.000% note rate. That gives context on the prospect of refinancing down the road.

It also clouds the refinance math on purpose. Knowing what we know in May 2026, a 6.375% market rate is lower than the original 7.00% note rate, but only a marginal improvement from permanent buydown rate of 6.625%. Since market rate improves the 7% rate more, we will end the analysis there.

That is the decision many buyers of new construction face in a locked in market.

First, What Is a Buydown?

In this example, a 2-1 buydown lowers the buyer’s payment temporarily. That is consistent with how temporary buydowns are treated in agency guidance. Fannie Mae describes temporary interest rate buydowns as a structure that reduces the borrower’s payment for a limited period of time. It is not contained to 2 years and could be longer or shorter.

No matter the period, it does not lower the actual note rate! No matter how long and how far below the note rate, your amortization stays with the start rate.

The caveat is the lower payment feels good, but the lower payment is not causing the loan balance to fall faster. It’s strictly a payment subsidy.

The builder subsidy fills the gap between what the borrower pays and what the loan requires under the full note-rate payment. That is the the key to the game.

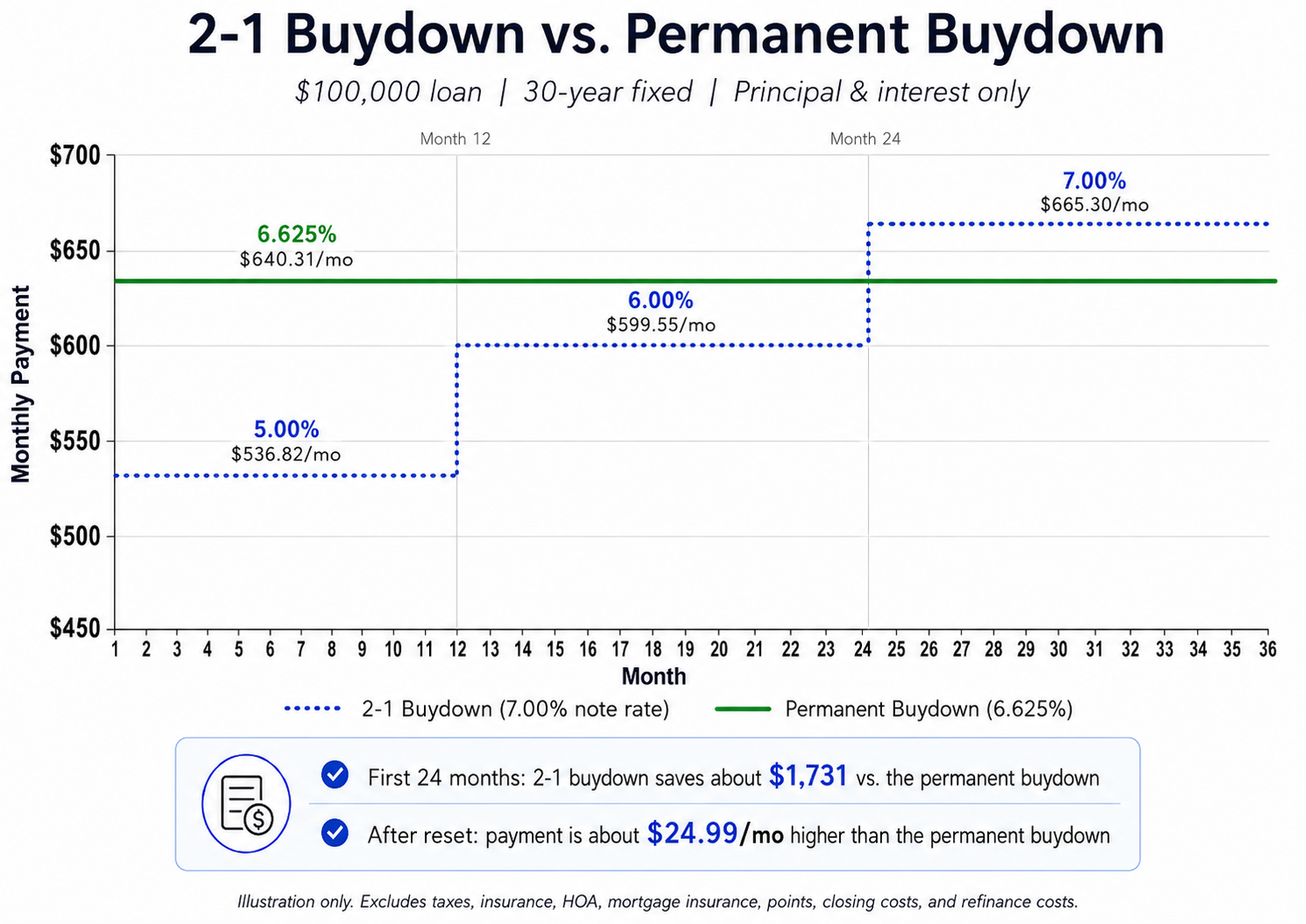

Monthly Payment Comparison

Come year three, if the buyer does not refinance, the payment becomes the full 7.000% note rate payment of about $665.

That distinction matters. It is the same reason I caution buyers not to look at monthly payment in isolation. Most important, you still have to qualify for the note rate payment. Next, payment is never the whole story. I covered that concept in more detail in this posts – Mortgage Calculator: Why Your Payment Isn’t the Whole Story.

The Builder Subsidy Behind the 2-1 Buydown

The 2-1 buydown works because the builder or seller funds the payment gap.

On this $100,000 example, the estimated subsidy would total:

| Subsidy Period | Approx. Subsidy |

|---|---|

| Year 1 subsidy | $1,542 |

| Year 2 subsidy | $789 |

| Total 2-1 subsidy | $2,331 |

The borrower feels the lower payment, but the loan receives the full payment stream required by the 7.00% note rate. So the buyer is not paying principal down faster. The buyer is receiving temporary payment assistance.

And here is the part that makes the math interesting.

Over the first 24 months, the total P&I applied to the loan is about $15,967. The total interest expense over that same period is about $13,862. The borrower’s reduced payments total about $13,636.

That means the borrower’s reduced 2-1 buydown payments do not even cover all of the interest expense during the first 24 months. The borrower-paid P&I is about $226 short of the interest expense.

The builder subsidy fills that gap and also supports the principal reduction required by the full note-rate amortization.

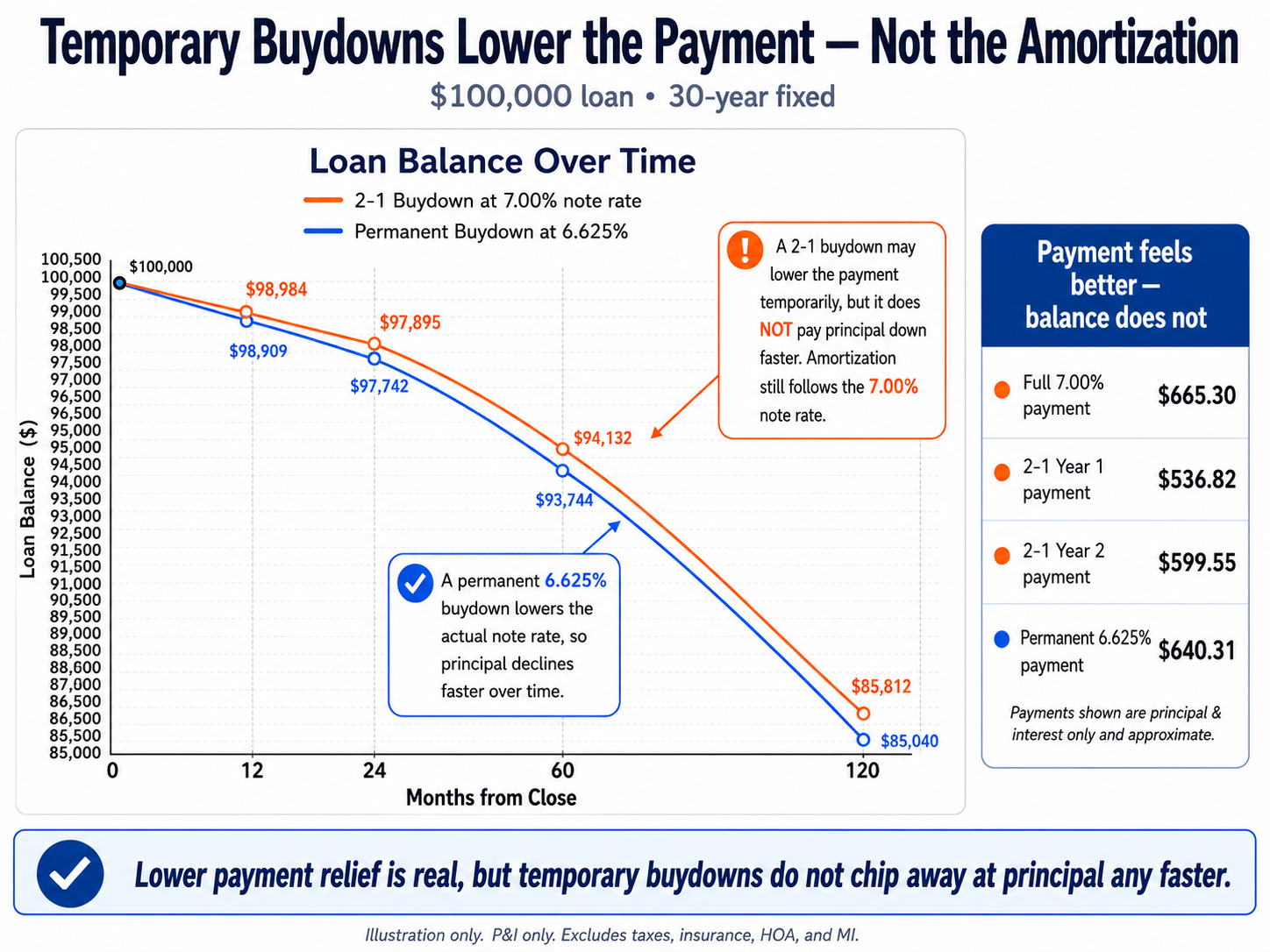

Temporary Buydowns Lower the Payment, Not the Amortization.

This is where the confusion sets in. The 2-1 buydown payment is lower, but the loan balance still follows the 7.000% note rate. A permanent buydown, on the other hand, actually lowers the note rate. That is why the permanent buydown balance declines slightly faster over time.

Two years later, the 2-1 buydown loan balance is about $97,895. The permanent buydown balance is about $97,742. Huh?

That difference is not huge on a $100,000 loan, but scale it on a $1,000,000. On any multiple, the larger the loan, the larger the gap.

What Happens (Next) After Two Years?

After 24 months, the 2-1 buydown period is over. No more subsidy, but two separate questions. The first question is whether the 2-1 buydown helped the buyer with cash flow. That answer is yes. The second question is whether the 2-1 buydown helped the buyer build equity faster. That answer is no.

At the two-year benchmark, the permanent buydown has a slightly lower balance because it lowered the actual note rate from day one.

| Scenario at 2 Years | Interest Expense | Total P&I Applied | Loan Balance |

|---|---|---|---|

| 2-1 buydown @ 7.000% | $13,862 | $15,967 | $97,895 |

| Permanent rate @ 6.625% | $13,110 | $15,367 | $97,742 |

The 2-1 buydown gave the buyer lower out-of-pocket payments during those first two years. But the permanent buydown still produced the lower balance and lower interest expense.

What If the Buyer Refinances in May 2026?

Now let’s assume the buyer took the 2-1 buydown in May 2024 and refinanced after the buydown expired in May 2026 at the market rate. This is hard to time, but you get the point.

| Scenario | Payment Rate | Approx. Monthly P&I |

|---|---|---|

| 2-1 buydown year 1 | 5.000% | $536.82 |

| 2-1 buydown year 2 | 6.000% | $599.55 |

| Full note payment | 7.000% | $665.30 |

| Permanent buydown | 6.625% | $640.31 |

| Refinance after 24 months | 6.375% | $638.30 |

The original loan balance after 24 months is about $97,895.

If the borrower rolls $2,000 of refinance costs into the loan, the new loan balance becomes about $99,895.

At a new rate of 6.375%, but keeping the same amortization, over the remaining 28 years, the new payment is around $638.

That is better than the original full 7% note payment of $665.

But the monthly savings is only about $27.

That means the simple payment break-even on $2,000 of financed refinance costs is roughly 74 months, or a little longer than six years.

That does not mean the refinance is wrong. It means the borrower needs to be staying in the loan, and home, long enough for the math to matter. The Federal Reserve’s consumer guide to mortgage refinancing explains why refinance costs and the break-even period matter when deciding whether to refinance.

So in a range bound market over the past few years, its a tough call.

Refinancing from 7.00% to 6.375% helps. But if the alternative was a permanent 6.625% buydown from the beginning, the refinance is not a huge payment improvement. And when the payment does not make sense, that could push out a refinance all together.

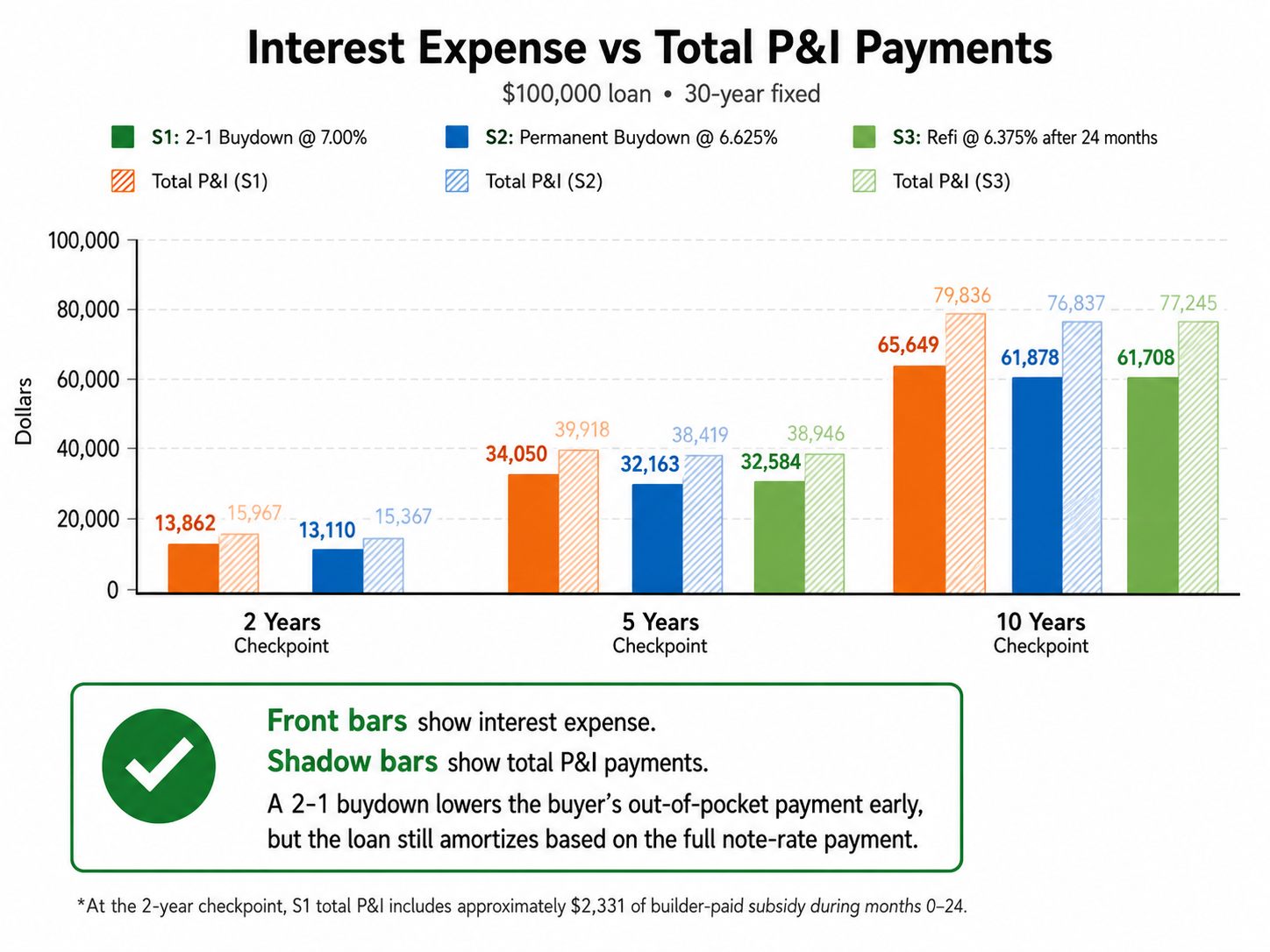

Two-Year Checkpoint

This graph compares interest expense and total P&I payments at the 2-year, 5-year, and 10-year checkpoints. The solid bars show interest expense. The lighter shadow bars show total P&I payments applied to the loan.

For the 2-1 buydown, the first two years include a builder subsidy. That is why the 2-year total P&I applied to the loan is higher than what the borrower paid out of pocket. A temporary buydown changes who makes part of the payment early on. It does not change the amortization math.

Five-Year Checkpoint

At the five-year mark, the refinance path begins to help compared with staying at the original 7% note rate. But the permanent buydown holds its own.

| Scenario at 5 Years | Borrower-Paid P&I | Interest Expense | Total P&I Applied | Loan Balance |

|---|---|---|---|---|

| 2-1 buydown, no refinance | $37,587 | $34,050 | $39,918 | $94,132 |

| Permanent buydown at 6.625% | $38,419 | $32,163 | $38,419 | $93,744 |

| 2-1, then refi to 6.375% after 24 months | $36,615 | $32,584 | $38,946 | $95,638 |

The refinance path has the lowest borrower-paid P&I through five years because the buyer had two years of payment subsidy and then refinanced to a lower payment.

However, the permanent buydown has the lowest interest expense and the lowest loan balance.

The refinance path looks good from a cash-flow standpoint, but the financed closing costs push the loan balance higher. At year five, the refinance balance is about $95,638. The permanent buydown balance is about $93,744. That is nearly $2k more debt on the refinance path.

Ten-Year Checkpoint

At the 10-year mark, the refinance path has had more time to work.

| Scenario at 10 Years | Borrower-Paid P&I | Interest Expense | Total P&I Applied | Loan Balance |

|---|---|---|---|---|

| 2-1 buydown, no refinance | $77,506 | $65,649 | $79,836 | $85,812 |

| Permanent buydown at 6.625% | $76,837 | $61,878 | $76,837 | $85,040 |

| 2-1, then refi to 6.375% after 24 months | $74,914 | $61,708 | $77,245 | $86,464 |

The refinance path finally shows the lowest cumulative interest expense, but only by a small amount compared with the permanent buydown. In this example, the refinance path has about $61,708 in interest expense compared with about $61,878 for the permanent buydown.

That $170 difference over 10 years but is a lot less than I expected.

Still the permanent buydown still has the lower loan balance. At year 10, the permanent buydown balance is about $85,040. The refinance path balance is about $86,464. Which means the refinance path has a balance that is about $1,424 greater, even though the rate after refinance is slightly lower.

Because the borrower financed $2,000 of refinance costs back into the loan. All the more important to run a break even analysis.

So Which Strategy is the Best?

All depends on what problem the buyer was trying to solve.

If the buyer needed lower payments in the first two years, the 2-1 buydown helped the most. It gave real payment relief when the buyer first moved into the home. Closing costs and prepaids are just the start of the long term conversation on capital needed to buy a home.

If the objective was the cleanest long term amortization, the permanent buydown helped more. It lowered the actual note rate from the beginning, kept the balance lower, and reduced the benefit to refinancing later.

However, if the buyer took the 2-1 buydown and refinanced after two years, the strategy was not bad. It improved the payment compared with sticking with the 7% rate. It also eventually caught up on interest expense. But it did not clearly beat the permanent buydown once you account for the higher loan balance created by financing the refinance costs.

The Refinance Math Is Close on Purpose

The fudging on the perm buy-down rate was intentional. Given the permanent buydown rate of 6.625% and lower rates today sheds color on the prospect of lower rates. After all, that is what the market expected under the new regime.

If rates had fallen to 5.75% or 6%, the refinance path would look much stronger. But in a range bound market, where rates grind slowly lower instead of collapsing, the permanent buydown remains competitive.

That is why buyers should not assume that a 2-1 buydown plus a future refinance will automatically win. It depends on how far rates fall, for how long, the hard costs, and ultimately how long the borrower keeps the new loan.

Practical Rules for Buyers

Understand that a buydown is a payment bridge. Versus a permanent buydown, is more rate strategy. A refinance is an opportunity, not a guarantee.

If the builder offers incentive dollars, do not look only at the year-one payment. Ask what the same incentive does if it is used for a permanent buydown. Then compare that to a realistic refinance plan.

As with a refinance plan, the question should not be, “is the new rate lower?” Rather, “is the new rate low enough to overcome the refinance costs and improve my position for the plan for the home?”

In this example, refinancing from 7.00% to 6.375%, matching the amortization, lowers the payment by about $27 per month. That helps, but with $2,000 in financed costs, it is not an immediate slam dunk. Check the math on a new 360 month term and see if that makes the math more appealing.

What I Would Do Now?

In a choppy 6% to 7% market, I would start by asking for the full builder incentive menu in writing. I would want to see the temporary buydown option, the permanent buydown option, the closing-cost credit option, and if they are open to a price reduction alternative.

Then I would compare the options across the board.

For a buyer planning to sell or refinance quickly, payment relief may matter most. If the loan is paid off before the expiration of the buydown, those funds get credited towards the loan payoff. That aspect can help a great deal if you think rates are going to move down quickly.

However, for a buyer planning to hold the loan for five years or longer, I would pay very close attention to the permanent buydown. If the builder incentive can permanently lower the rate in a meaningful way, perhaps more than 0.25%, that may be a winning strategy.

For a buyer who took the 2-1 buydown and is now looking at a refinance, I would not refinance just because the rate is lower. I would run the break-even calculation first. I would also compare more terms than just 30 years. Also, I would compare the fixed rates to the adjustable rate options too.

You can test that part here: Borrow Buy Build Refinance Calculator. That calculator is a good fit for this exact question because the refinance only makes sense if the payment savings justify the cost over the time you expect to keep the loan.

Famous Last Words?

The two year rate rewind shows exactly why builder incentives need to be matched to the buyer’s timeline. The 2-1 buydown gave real payment relief in a market that is still holds on to a six-handle. The permanent buydown gave cleaner long-term amortization. The refinance path helped, but it did not create a huge win because rates did not collapse. It likely made sense to ride out the payment subsidy while rates fluctuated.

Lower rates are inevitable, but they may come gradually. Its going to depend on inflation, not the Fed Chair. A good mortgage strategy should mirror the time in the loan and in the home.

So before choosing a builder incentive, ask a lot of questions. Then run the numbers, all of them!