A low home appraisal can derail a deal in minutes. You negotiate a price, complete a home inspection, and then the appraisal comes in under contract. Suddenly, you face an appraisal gap and a hard question: who covers the difference; the buyer, seller, or both?

The fact of life is that an appraisal doesn’t reveal a “hidden number.” Instead, it delivers a regulated opinion of value based on market evidence. Because appraisers interpret the evidence, two professionals can look at the same home and still reach different conclusions. In fact two appraisals are customary especially with custom or luxury properties.

A real example: two appraisals, two very different outcomes

On a recent high dollar transaction, the size of the loan request required a second full appraisal. The first appraiser landed at $2.9 million. The second came in at $2.45 million, a $450,000 gap on the same home.

So what causes that kind of disparity? In most cases, it comes down to two things:

-

Comp selection, and

-

Adjustments used to reconcile the comps.

First, what an appraisal actually is

An appraisal is an opinion of value, not a fact. Appraisers follow standards (like USPAP) and lender rules, but they still make judgment calls. That human element creates variance. In other words, the “mad science” shows up where interpretation begins.

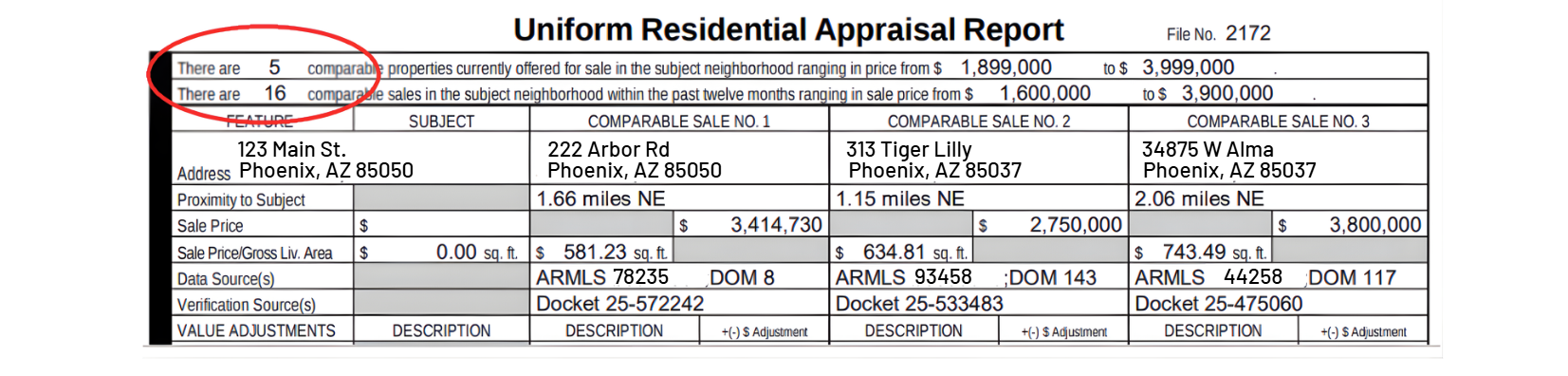

Step one: how appraisers “bracket” the market

Before an appraiser picks the best comps that end up on the report, they usually “bracket” the market. For example, the URAR often summarizes:

-

how many comparable homes are listed in the area and their price range

-

how many comparable homes sold in the last 12 months and their price range

This matters because it shows the pool of evidence the appraiser used. If the pool is thin, value can swing more. But, if the pool is deep, the conclusion usually tightens.

The comp selection rules most appraisers follow

Most appraisers use the same criteria. However, the final value still depends on which comps “win” and which ones get excluded.

1) Proximity: closer comps usually win

When two comps look similar, the one closer to the subject usually carries more weight. For example, if one comp sold 0.5 miles away and another sold 1.5 miles away around the same time, the closer one often wins – assuming the homes truly match.

2) Closed sales: recorded wins over “for sale”

Appraisers lean on closed, recorded sales because those reflect real buyer decisions. Meanwhile, active listings help as context, but they don’t prove value. Often appraisers will include a listing that is used to sample the current market. However, a listing cannot be used a legitimate comp since its not closed and recorded.

3) Recency: newer is better (typically within 12 months)

Appraisers typically use sales within the last 12 months. Even more important, they prefer recent comps because those reflect today’s market.

4) Bracketing GLA: one smaller, one bigger, one most similar

Appraisers try to bracket the subject’s gross living area (GLA):

-

one comp smaller than the subject

-

one comp larger than the subject

-

one comp closest in size and overall feel

That bracket helps support the final reconciliation.

5) Property type: compare like with like

Appraisers compare condo to condo and single-family detached to single-family detached. Otherwise, the buyer pool changes and pricing changes with it.

Bottom line: Appraisers follow a similar framework. So when values differ, comp selection and adjustments usually explain it.

Step two: adjustments create the biggest gaps

After the appraiser determines the comps, they adjust for differences: size, condition, quality, view, lot, upgrades, and layout. Even with the same comps, two appraisers can adjust differently. As a result, you can see large spreads especially at higher price points. Appraisers will usually write in the comments on their comp selection.

What to do when the appraisal comes in low

A low appraisal doesn’t automatically kill a deal. Instead, it forces a decision. Here are the most common options.

Option 1: Renegotiate the price

If the appraisal looks defensible, renegotiation often solves the problem fastest.

Option 2: Split the difference

Many deals survive when both sides share the gap. This keeps momentum and protects timelines.

Option 3: Cover the gap with cash

Sometimes the buyer chooses to bring the difference. However, that only makes sense if the home’s long term value or uniqueness justifies it. The lender will use the lower of the sales price of the home value.

Option 4: Request a Reconsideration of Value (ROV)

If the appraisal contains errors or missed stronger comps, you can request an ROV through the lender. The CFPB explains that borrowers may challenge inaccurate valuations through the ROV process.

To improve your odds, keep it factual:

-

submit 3 to 5 better comps (recent, close, truly similar)

-

document upgrades with dates, costs, and pictures

-

point out objective errors (GLA, bed/bath, amenities)

-

note concessions that inflated or distorted a comp

Additionally, the FHFA has published guidance related to ROV policies for the Enterprises. For deeper regulatory context, you can reference the Interagency guidance on reconsiderations of value.

The takeaway

A low appraisal feels personal. However, it usually isn’t. Appraisers make value by selecting comps and applying adjustments. Therefore, your best move is to understand their framework, then respond with better evidence, quickly!

If you want help navigating an appraisal gap or planning next steps, connect for a free consultation.