Pay Points or Reduce Price? True Mortgage Saving?

In the dance of a real estate purchase, homebuyers often find themselves at a crossroads involving seller concessions: is it better to pay points or reduce the price? If a seller is willing to offer concessions, what is the most advantageous way to accept and apply them?

The choice typically boils down to two options: a straightforward reduction in the property’s purchase price or a credit used to permanently buy down the mortgage interest rate. While a lower sticker price offers immediate psychological satisfaction, a careful mathematical analysis often reveals a different path to long-term financial impact.

For the majority of buyers in this market, directing seller concessions toward a rate buydown can yield superior financial benefits; primarily by securing a lower, more manageable monthly payment for the foreseeable future.

Why this decision matters

This post provides a quantitative framework for understanding this crucial decision. By examining how each choice impacts a buyer’s monthly obligation and overall financial picture, we can see when a lower rate can outperform a token price cut.

If you want to run your own scenarios, use the Borrow Buy Build 4-Way Calculator to solve for your optimal payment, loan amount, term, or interest rate.

The core calculation behind the monthly payment

The heart of this analysis lies in the composition of a mortgage payment, which is primarily principal and interest. The two “levers” that drive your P&I payment are:

-

Loan amount (directly affected by price and down payment)

-

Interest rate (directly affected by points / buydowns)

Both a price cut and a rate buydown can lower a payment, but their impacts are not always equal. Understanding how each lever behaves is the first step toward making an informed decision.

Option 1: Reduce the purchase price

A price reduction directly lowers the principal balance of the loan. However, it’s crucial to recognize that the reduction in the loan amount is not the full amount of the price cut. Check out how price reductions are impacting the new home market in the US.

It’s the price cut minus your down payment percentage. For example, on a home with a $10,000 price reduction, a buyer putting 20% down will see their loan amount decrease by only $8,000, because the remaining $2,000 would have been covered by their down payment.

Example: price cut impact on payment

Consider a $400,000 loan (representing a $500,000 purchase with 20% down) at 6.50%.

An $8,000 reduction in loan principal (from a $10,000 price cut) results in monthly savings of approximately $51 per month. Helpful, but this becomes our baseline for comparison.

Option 2: Use concessions to pay points and buy down the rate

Alternatively, a seller credit can be used to pay for discount points, which are prepaid interest paid at closing in exchange for a lower interest rate. This strategy is commonly called a permanent buydown.

The benefit here is simple: even small rate reductions can create meaningful payment relief—especially on larger loan amounts.

Example: a modest rate drop impact on payment

Using the same $400,000 loan, let’s analyze a 0.25% rate reduction, from 6.50% to 6.25%.

That change results in monthly savings of approximately $65 per month—nearly 30% more monthly savings than the $10,000 price cut example.

For a quick roundup of other mortgage tactics buyers use today, you can reference that Yahoo! mortgage “hacks” article you mentioned.

Side-by-side comparison: points vs price reduction

The consistent outcome in many cases is that a lower rate provides a larger reduction in monthly payment—improving affordability and often helping debt-to-income ratio (DTI) as well.

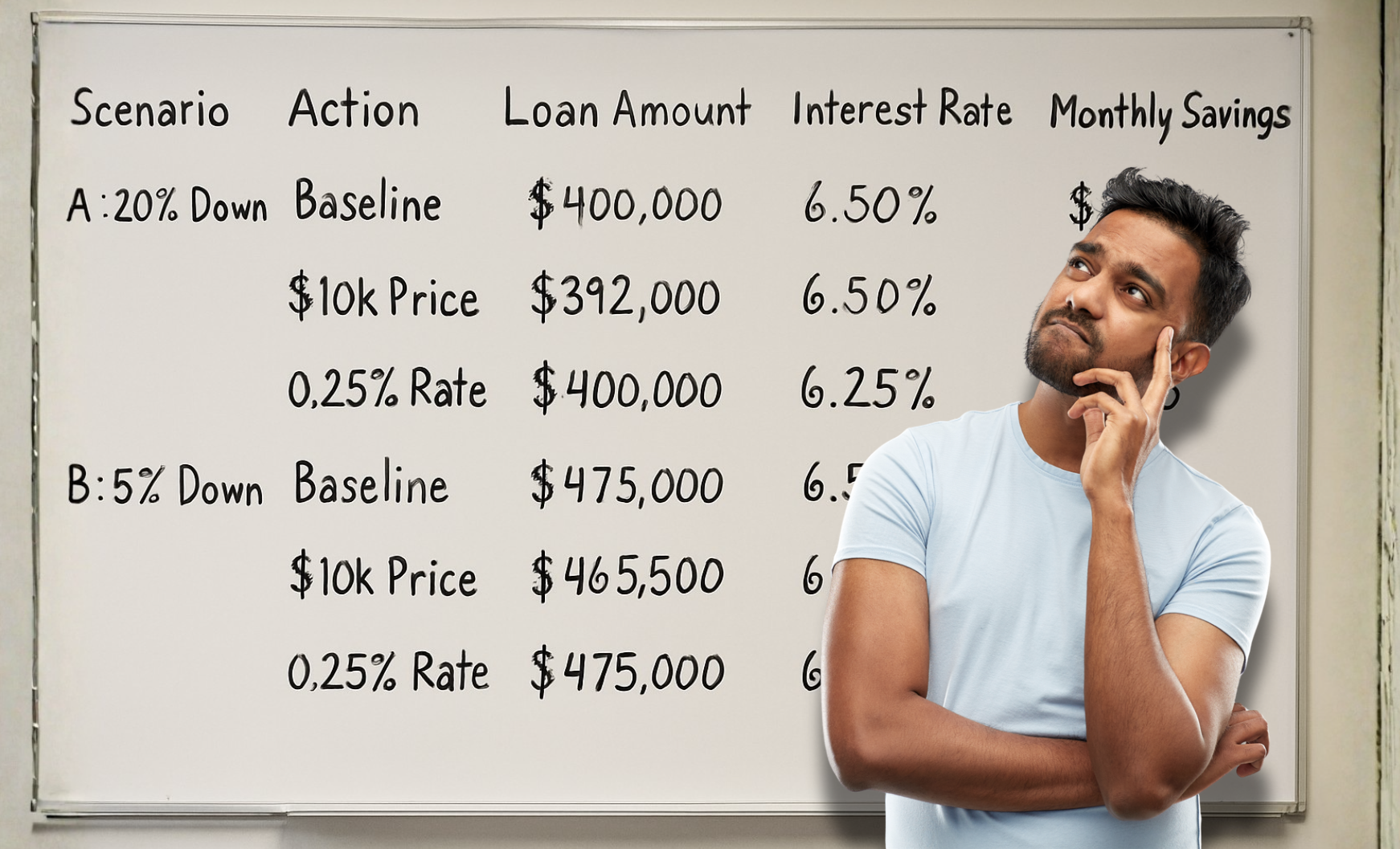

Scenario A: 20% down

| Scenario | Action | Loan Amount | Interest Rate | Monthly P&I | Monthly Savings |

|---|---|---|---|---|---|

| A | Baseline | $400,000 | 6.50% | $2,528 | — |

| A | $10k Price Cut | $392,000 | 6.50% | $2,477 | $51 |

| A | 0.25% Rate Drop | $400,000 | 6.25% | $2,463 | $65 |

Scenario B: 5% down

| Scenario | Action | Loan Amount | Interest Rate | Monthly P&I | Monthly Savings |

|---|---|---|---|---|---|

| B | Baseline | $475,000 | 6.50% | $3,002 | — |

| B | $10k Price Cut | $465,500 | 6.50% | $2,942 | $60 |

| B | 0.25% Rate Drop | $475,000 | 6.25% | $2,924 | $78 |

Should you pay discount points or negotiate a lower purchase price?

When you have $10,000 in seller concessions, the choice to pay points or reduce price becomes a measurable decision.

A buyer could apply the credit toward price, lowering the mortgage amount and saving around $51/month in the 20% down example. But if that same $10,000 is used to purchase points, the payment impact may be stronger.

A practical points framework

Points pricing changes daily, but here’s a basic guideline many buyers use when comparing options:

-

1 point = 1% of the loan amount

-

Often, 1 point can buy roughly 0.25% in rate (varies by day, loan type, credit, occupancy, etc.)

So, on a $400,000 loan, $10,000 could be around 2.5 points. Depending on market pricing, that may create something like a 0.50% rate reduction.

That’s why concessions used for points can feel like “more leverage”: you’re using the seller’s money to reduce your payment every month.

When reducing the price makes more sense

A rate buydown isn’t always the winner. Here are cases where a price reduction can be the smarter move.

Cash-to-close constraints

If your limiting factor is the cash needed for down payment, closing costs, and reserves, then a lower price may reduce required funds and help you get to the table, especially if reserves are tight.

Monthly payment is one part of qualifying; required cash is another.

Short time horizon

If you expect to sell or refinance within a few years, the long-term savings from points may not have enough time to “pay you back.”

Points are prepaid interest. If you don’t hold the mortgage through the breakeven period, it can become a sunk cost.

Unfavorable market for points

On certain days, the market pricing for points can be expensive. If the buy-down cost is high, the advantage can shrink.

In those cases, it’s smart to compare alternatives like:

-

adjustable-rate mortgages (ARMs)

-

temporary buydowns (if available and appropriate)

-

waiting for a better pricing day if timing allows

A framework to boost affordability

For the buyer focused on long-term affordability and payment optimization, prioritizing a permanent rate buydown over a price reduction can be a powerful strategy.

A clean way to think about it:

-

Use price negotiations to solve for value and equity position

-

Use seller concessions to solve for affordability and monthly payment

When you approach negotiations with data comparing each strategy side by side so you can turn a home purchase into a true financial win: not just getting into the home, but staying comfortable in it.